Modelling censored losses using splicing: A global fit strategy with mixed Erlang and extreme value distributions

Abstract

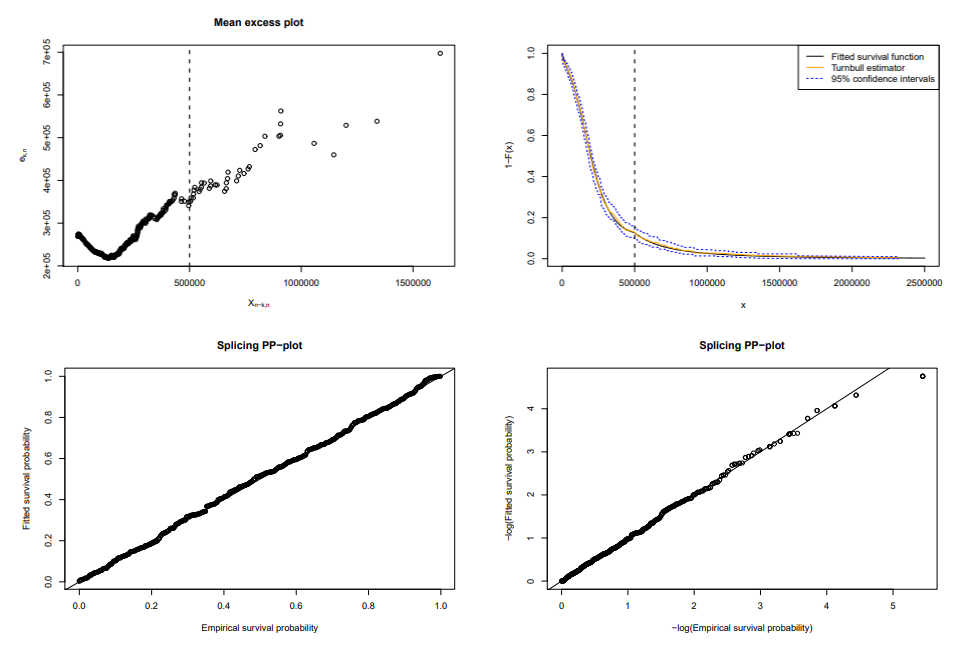

In risk analysis, a global fit that appropriately captures the body and the tail of the distribution of losses is essential. Modelling the whole range of the losses using a standard distribution is usually very hard and often impossible due to the specific characteristics of the body and the tail of the loss distribution. A possible solution is to combine two distributions in a splicing model: a light-tailed distribution for the body which covers light and moderate losses, and a heavy-tailed distribution for the tail to capture large losses. We propose a splicing model with a mixed Erlang (ME) distribution for the body and a Pareto distribution for the tail. This combines the flexibility of the ME distribution with the ability of the Pareto distribution to model extreme values. We extend our splicing approach for censored and/or truncated data. Relevant examples of such data can be found in financial risk analysis. We illustrate the flexibility of this splicing model using practical examples from risk measurement.